Realty Income is deploying capital at a 235bps spread over its 4.75% borrowing cost — the widest in five years — while 671 consecutive monthly dividends, AFFO growing 6.6% YoY, and a private capital platform with Apollo and GIC are being completely ignored by the ‘rate-sensitive REIT’ label.

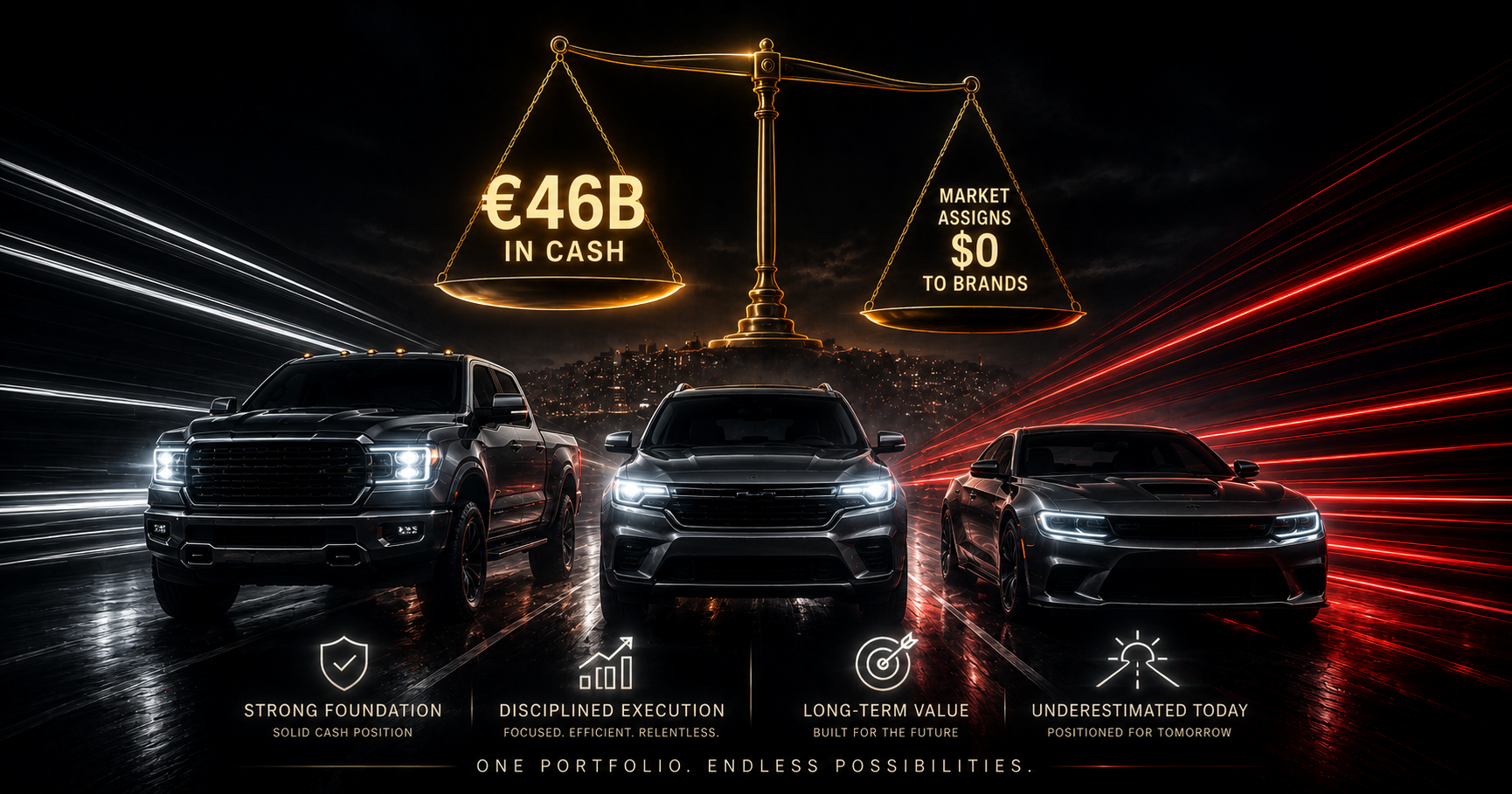

Stellantis’ $38B market cap is below its €46B industrial liquidity, implying 14 global car brands, 40 factories, and 288,000 employees are worth less than nothing. Q1 2026 returned to profitability under CEO Filosa with 12% volume growth — North America leading.

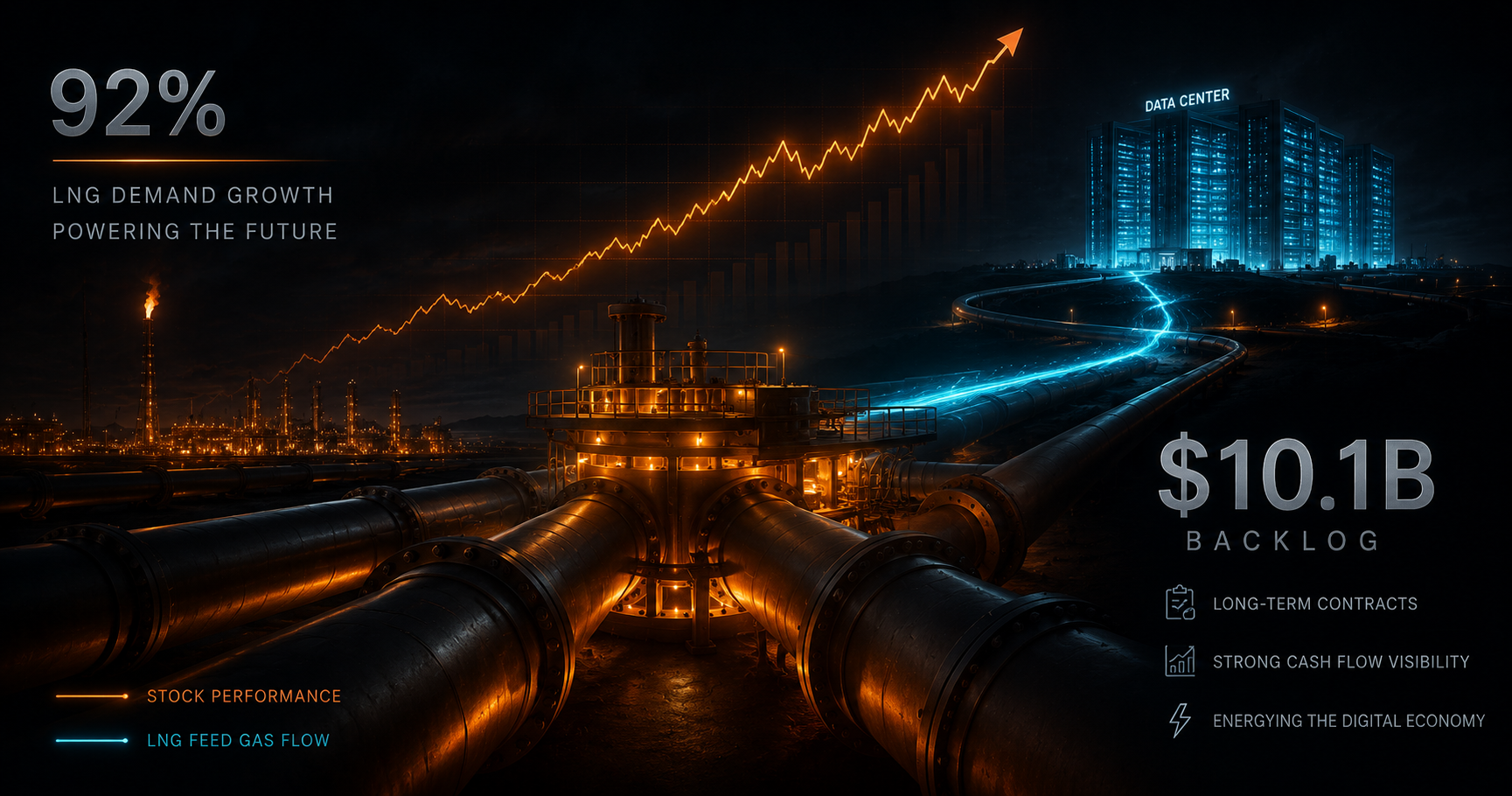

Kinder Morgan beat Q1 2026 EPS by 41% on LNG feed gas deliveries and data-center-driven power demand — not cold weather. With 10+ Bcf/day of power projects under development, a $10.1B contracted backlog, and a Moody’s credit upgrade, KMI is re-rating toward regulated utility multiples.

Realty Income is deploying capital at a 235bps spread over its 4.75% borrowing cost — the widest in five years — while 671 consecutive monthly dividends, AFFO growing 6.6% YoY, and a private capital platform with Apollo and GIC are being completely ignored by the ‘rate-sensitive REIT’ label.

Stellantis’ $38B market cap is below its €46B industrial liquidity, implying 14 global car brands, 40 factories, and 288,000 employees are worth less than nothing. Q1 2026 returned to profitability under CEO Filosa with 12% volume growth — North America leading.

Kinder Morgan beat Q1 2026 EPS by 41% on LNG feed gas deliveries and data-center-driven power demand — not cold weather. With 10+ Bcf/day of power projects under development, a $10.1B contracted backlog, and a Moody’s credit upgrade, KMI is re-rating toward regulated utility multiples.

General Mills’ Q4 FY2026 adjusted EPS beat consensus by 15.9% and the company launched a $3B cumulative cost savings program — both buried under a $2.1B non-cash goodwill impairment. The real business is inflecting positively; the GAAP headline is accounting noise.

Humana’s Q1 2026 operating cash flow surged 278% to $1.25B, confirming the Medicare Advantage actuarial crisis is stabilizing — while 22% membership growth and a CenterWell platform valued at zero in consensus models point to a trough-earnings setup with $25+ EPS by 2028.

Verizon posted its first positive Q1 postpaid adds since 2013. Frontier fiber convergence yields 30% lower churn on bundled customers, backed by a 6.1% yield and 21 consecutive annual dividend raises.

Apollo posted record $728M Fee Related Earnings and crossed $1 trillion in AUM in Q1 2026. A 40-60% valuation discount to peers versus 30% FRE growth makes no fundamental sense.

Kraft Heinz's 7.1% dividend yield is pricing in a cut that 1.9x free cash flow coverage doesn't support. New CEO Steve Cahillane's $600M investment cycle follows the same playbook that worked at Kellogg's.

Boeing's Q1 2026 deliveries exceeded Airbus for the first time since 2019, backed by a record $695B backlog and a production ramp from 42 to 47 aircraft per month that turns free cash flow decisively positive.

CVS Health's Q1 2026 Aetna medical benefit ratio of 84.6% and five consecutive earnings beats confirm the turnaround is structural, not seasonal. Caremark's 11% revenue growth and 200bps GLP-1 share gain are the hidden growth engine.

AT&T's 45% fiber-to-wireless attach rate and a quantified $6.5-8.0B OBBBA tax tailwind are accelerating deleveraging — while the market still prices T as a debt-overhang story.

Citigroup's Q1 RoTCE of 13.1% already cleared its 2026 target, and the bank is buying back stock near tangible book value of $99.01 — yet it still trades like an unfinished turnaround.

Dow's Q1 beat and Q2 guidance raise to $2.2B operating earnings signal the chemicals cycle has bottomed — while European plant rationalization permanently removes supply the Street's oversupply thesis hasn't priced in.

Conagra's 11% dividend yield is pricing in a B&G Foods-style halving — but Conagra runs at 3.8x leverage versus B&G's 6-8x, and Q3 organic sales just returned to growth led by Frozen and Snacks.

Pfizer's April 2026 patent settlements quietly pushed the Vyndaqel franchise cliff from 2029 to mid-2031 — while a 39%-growing Padcev franchise and a hidden obesity option in Metsera remain priced near zero. The market hasn't caught up.

PYPL has de-rated to ~$44 and ~8.4x earnings on a single fear — branded checkout is losing share — while consensus misprices three things the filings refute: a ~$14B transaction-profit base growing 3% in spite of the checkout drag, a Venmo/PSP growth engine compounding double digits, and a ~$6B annual buyback retiring ~10% of the float a year. Forensic case: BUY, $62 in 12 months, $80+ long-term.

Altria has re-rated 27% to ~$72, yet still trades at 13x against a 19x historical average while consensus prices three demonstrably wrong calls: a "volume cliff" offset by relentless pricing power, a smoke-free option marked near zero after NJOY, and a ~$9B ABI stake buried by single-multiple math. Forensic case: BUY, $82 in 12 months, $95+ long-term.

BMY trades at 9.3x P/E and a 4.5% yield while three forensic mispricings sit in plain sight: the Eliquis IRA cliff that didn't happen, a growth/legacy crossover already cleared in 2025, and a $14B Cobenfy option the Street is valuing at zero. Rating: BUY. 12-month target $78, multi-year intrinsic $95+.

Hershey trades at 19x forward earnings versus a 10-year median of 26x, while consensus prices in three demonstrably wrong assumptions about cocoa, GLP-1s, and Salty Snacks. The forensic case points to $235 in 12 months and $275+ longer term.

Option 2 — Contrarian hook

The market thinks GLP-1s will hurt chocolate demand — peer-reviewed Cornell data shows the opposite. Combined with the cocoa hedge lag and an unmodeled Salty Snacks asset, Hershey's mispricing is measurable, falsifiable, and worth 25%+ upside.

· 15 min read

—

—

—

Loading…

Get new research in your inbox

Forensic equity research on US stocks. No spam, unsubscribe anytime.

O

O